Property prices returned to a growth trajectory in 2024 and 2025 following a previous correction. Despite this upward trend, mortgage market activity has rebounded this year. New loan volumes in 2025 are among the strongest seen in the last three years, with rates stabilizing at around 4.5–5%—a level most analysts now consider the new long-term standard.

At the same time, as we close out 2025, we already know that 2026 will bring:

- A more stable macroeconomic environment,

- A continued limited supply of new housing,

- Regulatory changes to investment mortgages, set to take effect in April 2026.

It is also highly likely that we will see continued growth in the rental market due to the inaccessibility of homeownership, alongside the ongoing impact of legislative and regulatory changes that are already affecting construction, mortgage limits, and pricing.

In the following sections, we will explore these individual areas: the economic environment, lending and interest rates, supply and demand, and regulation. There is plenty to unpack in each of these topics.

MACROECONOMIC INDICATORS

These are the factors that determine the purchasing power of Czech households, mortgage affordability, and investment behavior. What is influencing how the real estate market will behave going forward?

Inflation close to the CNB target

Forecasts from the Czech National Bank (CNB) and the Ministry of Finance project that inflation will sit close to the two-percent target by 2026. Prices will no longer put downward pressure on the real purchasing power of households—a significant shift compared to 2022–2023.

Stable inflation benefits the entire real estate market: the central bank doesn't need to make dramatic rate changes, keeping them within a predictable range instead. This allows households to better plan their mortgages, real incomes stop falling, and the market generally operates in a more stable environment.

Mild and stable economic growth

According to the CNB, the Ministry of Finance, the OECD, and the Chamber of Commerce, GDP is expected to grow at a rate of approximately 2–2.5% in 2026. While not a dynamic expansion, this growth is stable enough to support both housing demand and investment activity.

Crucially, the Czech economy will not enter 2026 in a recession or a period of significant macroeconomic uncertainty. This creates a much more predictable environment for the real estate market than we've seen in previous years.

Low unemployment as a pillar of demand

Unemployment is one of the best leading indicators of demand for homeownership. The unemployment rate (based on ILO methodology) remained stable throughout 2025, fluctuating between 2.6% and 3.2%. This keeps it at a level that has long been among the lowest in the European Union.

LENDING AND INTEREST RATE INDICATORS

Interest rates and credit availability dictate how much people can afford to borrow for housing—and consequently, how strong the demand for property will be. When conditions are stable, both households and banks can plan with much greater certainty.

More stable interest rates as the new standard

According to the CNB forecast, interest rates are expected to decline only gradually in 2026, staying in a range close to current mortgage rates—around 4.5% to 5%.

Crucially, neither the market nor the CNB anticipates a return to the extremely cheap credit seen in 2020–2021. Instead, most analysts view current levels as a new long-term trend, meaning buyers are no longer holding out for magically cheap mortgages.

This has several consequences:

- While mortgages remain expensive for some households, the rates no longer come as a shock.

- A low-volatility rate environment provides greater certainty for financial planning.

- Banks can manage risk more accurately and are lending more actively than they did in 2022–2023.

It is precisely this stability—rather than the rate level itself—that was the primary driver behind the mortgage market's strong recovery in 2025.

Rising mortgage market activity

What do the numbers say?

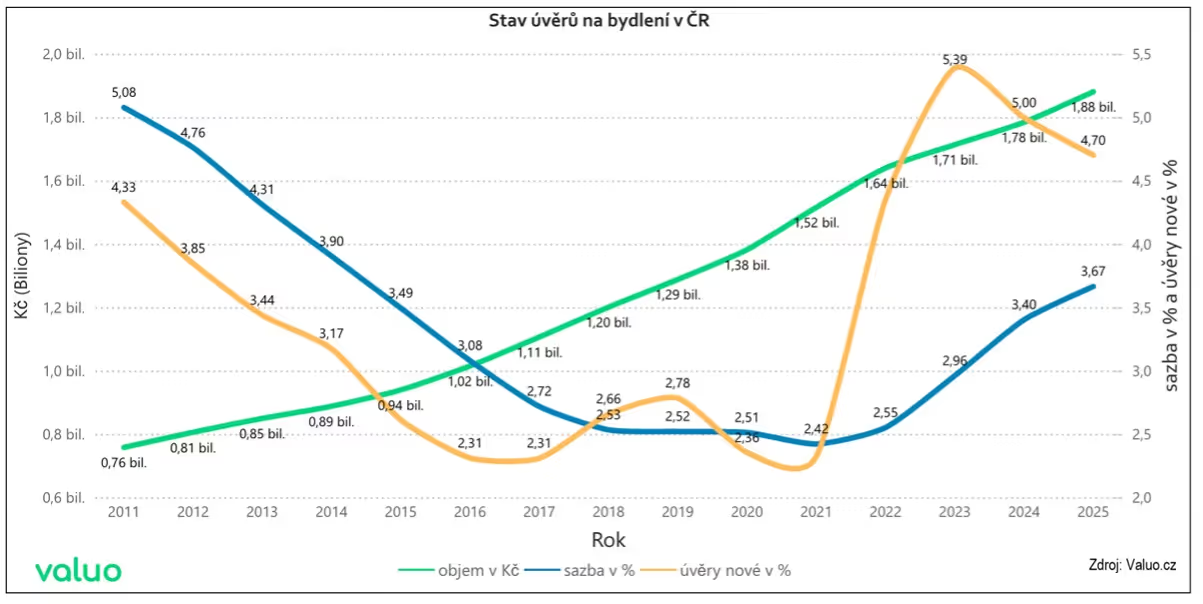

- Data from December 2025 shows an average offered rate of 4.91% p.a.—which, without any major fluctuations, is the lowest rate seen in the last three and a half years.

- Total mortgage volumes in 2025 reached an average of CZK 55 billion per month—more than in the exceptionally strong year of 2021.

- Driven by the growth of new mortgages, total household debt is also rising slightly, currently standing at CZK 1.88 trillion. It is growing by roughly CZK 110 billion annually.

One important detail is the average interest rate across all existing mortgages: 3.67%. This still reflects the low-rate environment of recent years, which cushions the impact of new, more expensive loans on family budgets.

Refinancing remains marginal

Switching lenders? In 2026, this will likely remain a relatively niche activity. The primary focus will be on new lending.

According to the CNB, refinancing accounts for less than a tenth of all mortgage loans. The reason is simple: rates are very similar across banks, so households have little incentive to switch providers.

Short-term rates as a key signal for the coming months

Short-term interbank rates—led by the 3M PRIBOR (the rate at which banks lend money to one another for three months)—answer the following question: how expensive is money in the economy right now?

Based on this indicator, the Czech National Bank anticipates short-term stability followed by a mild increase. As a result, mortgage rates are not expected to see any significant changes in the coming quarters.

TIP: You might be surprised by the Five trends that shaped the real estate landscape in 2025.

PROPERTY SUPPLY

The supply side of the market remains one of the biggest housing challenges in the Czech Republic. Although demand revived in 2025, new construction continues to lag, leaving the supply of new housing constrained even at the close of 2025.

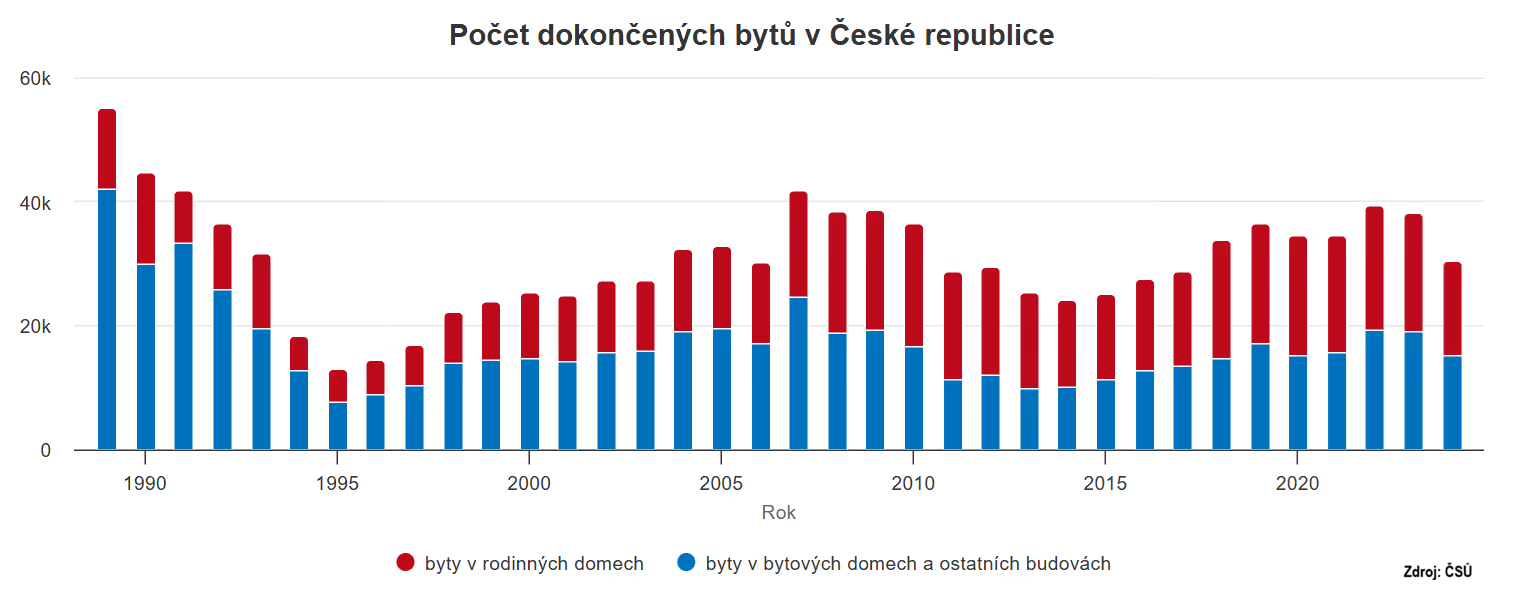

Following a roughly 18% year-on-year drop in completed flats in 2024, 2025 brought no significant change.

During the first three quarters, the number of completed flats remained almost exactly the same as in the same period the previous year. Construction is sluggish, flats sit at historic price highs, and overall supply is not growing. As a result, there is no reason to expect price growth to slow down significantly.

The Czech market is characterized by a long-term trend of construction lagging behind household needs. This creates an environment where any revival in demand immediately collides with a structural shortage of flats. This issue is most pronounced in large cities, where the situation translates into higher prices almost instantly.

And what do the numbers say?

- That the Czech Republic is among the EU countries with the slowest housing construction—in 2024, construction began on 27,198 flats.

- And that the market is entering 2026 with renewed asymmetry. On one side is a stabilized economy and stronger housing demand; on the other, a constrained supply that cannot adapt due to land shortages, planning restrictions, and high construction costs.

EMAND FOR PROPERTY IN 2026

The demand side of the market clearly revived in 2025. The volume of new mortgages nearly tripled throughout the year, stabilizing at around CZK 26 billion per month—making it one of the strongest results since 2021. These figures confirm that buyers are returning to the market, though not all for the same reasons or with the same motivations.

Demand in 2026 will be driven by two main groups:

Households seeking their own home

This group forms the primary engine of demand. Their decision-making isn't speculative; it stems from genuine life needs and the strong Czech preference for homeownership. Households might delay a purchase briefly, but not for years—and as soon as the economic environment calms down, they are the first to return to the market.

Several factors are contributing to their return:

- Inflation sitting near the two-percent target,

- low unemployment,

- and mild but stable wage growth.

TIP: Looking for a new home? Browse our property listings.

This group is highly sensitive to mortgage rates. Even small rate changes significantly affect housing affordability, which is why short fixed-rate periods of up to three years are the most common choice today, accounting for the vast majority of newly agreed loans—approximately CZK 20 billion out of the CZK 26 billion provided each month. This allows households to adapt if rates fall in the coming years.

Investors

Investment demand was stable in 2025, but not as pronounced as during the era of ultra-cheap mortgages. Investors are being more selective, paying closer attention to yields and specific locations.

Do roku 2026 však vstupují s novým omezením: Od dubna začnou platit přísnější podmínky pro investiční hypotéky na třetí a další nemovitost, konkrétně jde o maximální 70% LTV a DTI omezené na sedminásobek ročního příjmu. To zvýší nároky na vlastní kapitál a část investorů z trhu vytlačí.

Entering 2026, however, they face a new constraint: starting in April, stricter conditions will apply to investment mortgages for third and subsequent properties—specifically, a maximum LTV of 70% and a DTI limited to seven times annual income. This will increase equity requirements and push some investors out of the market.

The CNB recommendation is expected to affect only a small portion of the mortgage market; the central bank estimates it will involve up to 10% of new loans. Moreover, due to the supply-demand imbalance, financing is done in cash in roughly half of all cases.

How is the investment property game changing? Find out whether buying an investment flat still makes sense in 2026.

OVERALL FORECAST

The year 2026 is unlikely to bring any dramatic shifts, but rather a continuation of the trends already taking shape. The economy is stabilizing, mortgage rates are remaining within a predictable range, and the supply of new housing is limited. Household demand will continue to strengthen, investors will proceed more cautiously due to tightened regulations, and cash buyers will remain a key stabilizing force. The combination of these factors suggests that property prices will grow modestly in 2026 (up to 5%). This growth will be steady rather than rapid, particularly in areas where the pressure on housing affordability is highest.

Overall, the market is entering 2026 with greater predictability than in previous years. No return to extremes is expected; instead, we anticipate a period of gradual consolidation in which stable rates, limited construction, and a steady recovery of buyer confidence will play the leading roles.